HELP! My 401(k) Account is Down! What Should I Do?

Don’t panic!!! There’s a strong likelihood that you are not alone witnessing the fall in your retirement fund assets. I’d be willing to wager that just about anyone with a 401(k) plan—or other tax-advantaged defined contribution retirement plan—who is more than twenty years from retirement, is in the red for the first three months of this year. From its high in late February, the S&P500—one broad measure of the U.S. stock market—has fallen by more than 10%, a decline that is considered to be a “correction” in the market. It may not be of much consolation to realize that you have company in your misery; however, hopefully you will take some solace in the fact that, over the last 45 years, i.e. since the inception of the defined contribution industry, there have been numerous market corrections and even “bear markets”—defined as a stock market decline of 20% or more.

So—how do you answer that burning question, “What should I do?” Before answering that question, it’s key to keep in mind that your retirement account is most likely the longest term asset that you own. If you are thirty years old, and you anticipate retiring at the age of 65, you are de facto planning to hold that account for thirty-five years and then on into retirement. That is likely far longer than you will own a house. When you’re looking into the future some twenty or thirty years for returns on your retirement plan, it’s important not to panic. The short term vagaries in the stock market are part of the “cycle of life” in the world of investment. If you had been really “smart” and had predicted correctly that the market was going to fall 10% and had sold all the stocks in your retirement portfolio and invested the proceeds in cash, I would argue that you had been wonderfully “lucky.” You might congratulate yourself; however, that smart selling means that the job is only half done. You will then have to be “smart” (or lucky) a second time so that you get reinvested into the market before it rallies. There are people who spend their days engaging in short term buying and selling of their personal accounts. They are professional traders, and while some make good money in that career, many more do not. Most Americans with 401(k) plans have careers in a broad array of other industries and sectors of the economy; for them, short term volatility, while unsettling, should be put in the context of the long term horizon they must take to fund their retirements.

Here are a few basic precepts to keep in mind when the stock market is making you lose sleep at night. Most employees are paid every 15 days (or perhaps every two weeks). That is also when their 401(k) deductions are withdrawn from their payroll and invested into the fund options they have selected. It is also when the employee match is made by the employer, money that is added to the employee’s retirement account. If on payday the market seems to be crumbling, don’t panic. Rather, remember this: (1) you are averaging down when you buy stocks in a declining market; (2) the employer match, whether it is 2% or 4% or more, is found money; (3) if the employee invests the full amount of the employer match—e.g. 4% of gross revenue that is matched by a 4% contribution by the employer—the employee has instantaneously made a 100% return on their contribution; (4) over the long haul, the U.S. stock market return has been one of the best ways for individuals to build wealth and to enhance their retirement income.

So—what is roiling the stock market right now? Very simply, it’s economic uncertainty, driven by events that have taken place since the new administration was voted into office on January 20th. In particular, the imposition of tariffs on Canadian, Mexican and Chinese imports into the U. S.—with the threat of expanded tariffs by as early as April 2, on imports from numerous other countries—is having a negative impact on the outlook for both inflation and consumer demand, as the costs of tariffs are passed through to retail consumers. Coinciding with the tariff war is the ongoing layoff of Federal Government employees which is raising concerns of rising unemployment and slowing economic growth. The market is observing these challenges and reacting. It’s key to remember that the stock market is a forward-looking barometer of economic prosperity—the past is of no interest to stocks—and if the above-mentioned trends continue, the impact on corporate earnings growth is likely to be unfavorable. Thus, the current angst and turmoil in the prices of stocks. That said, there are still strong underpinnings to the U.S. economy, and it is not guaranteed that a recession is at all inevitable, particularly if the issue of tariffs can be resolved before too much damage is done. My pragmatism makes me optimistic, but not overly confident in a peaceful solution.

So—how does one try to manage through this maze of economic concerns when it comes to that long term asset that is your future retirement income? Let’s put the defined contribution history in perspective. The 401(k) market was spawned in 1978 by an act of Congress. Today, it is a more than $4 trillion behemoth, one that is highly regulated by the Federal Government—both the companies that manage the assets as well as the individuals who are portfolio managers as well as client service, marketing and sales representatives. In the intervening 47 years, the industry has developed an array of sophisticated products that cater to the needs of working people, enabling them to enhance their income in their “golden years.” Far and away, the most popular vehicle today in the toolbox of retirement fund options available to employees is the “Target Date Fund,” a product that is designed to take into consideration the age of each employee and each one’s propensity for risk. Their value lies in being highly concentrated in equities during the first few decades of an individual’s employment years, and reducing equity risk exposure as one nears retirement age. Virtually all companies’ defined contribution plans offer both target date funds and an array of other options that allow employees to make their own investment decisions. The product has proven to be a value-added investment when used by employees as a long term tool for building wealth.

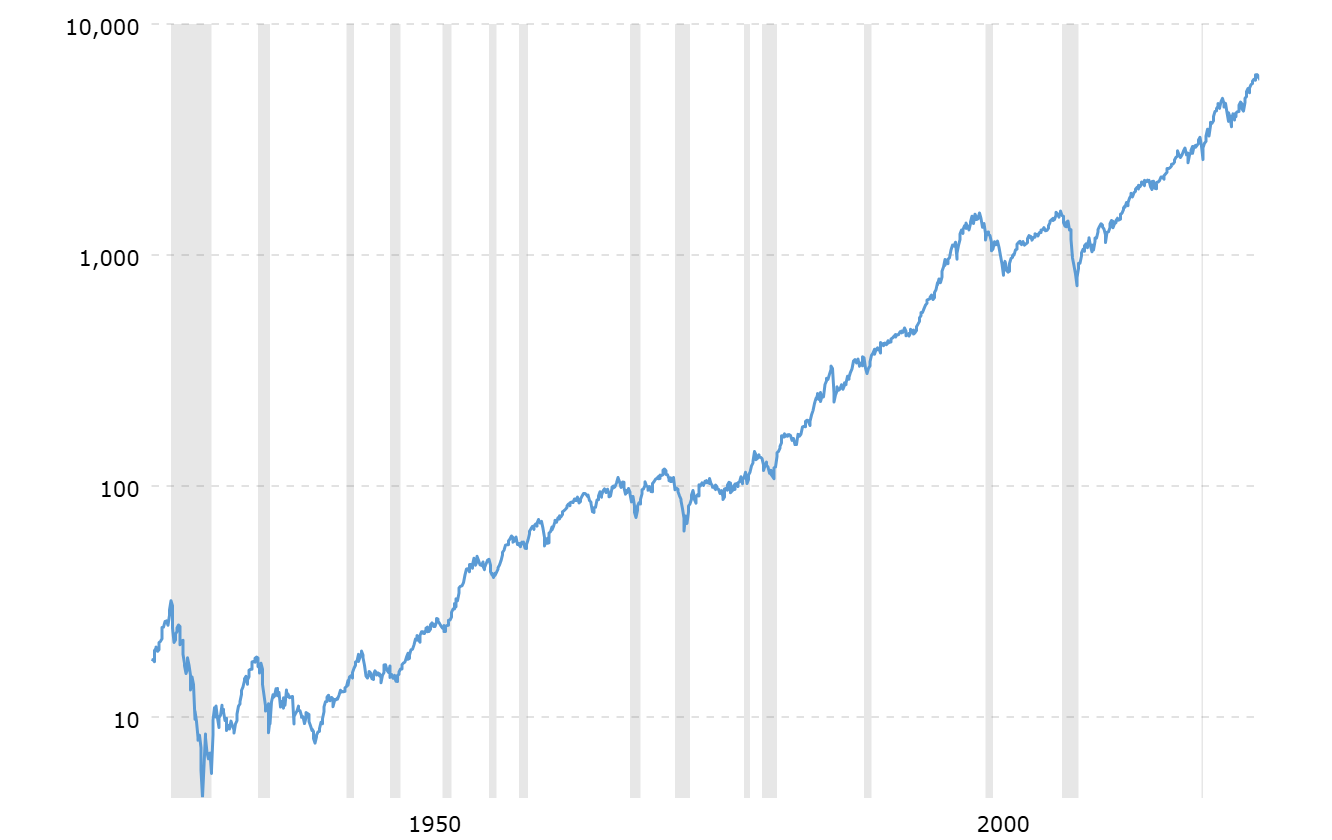

No one likes to lose money on investing, not even in the very short run. Maybe a picture of the long run can pick your spirits up when things seem tough. The attached chart is of the S&P500 over a period of 90 years. Look at each serious decline in the market and then what happened afterward. Despite the current dislocations, there is much to be optimistic about in the long term.